Bloomberg — Global inflation is finally coming off the boil, even if it’s set to remain far too hot for the liking of the world’s central bankers.

As economic growth slows, prices for key raw materials — from oil to copper and wheat — have cooled in recent weeks, taking pressure off the cost of manufactured goods and food. And it’s getting cheaper to move those things around, as supply chains slowly recover from the pandemic.

After the worst price shock in decades, the speed at which relief arrives will vary, with Europe in particular still struggling. But for the world as a whole, analysts at JPMorgan Chase & Co. estimate that consumer-price inflation will fall to 5.1% in the second half of this year — roughly half of what it was in the six months through June.

“The inflation fever is breaking,” says Bruce Kasman, the bank’s chief economist.

That doesn’t mean an early return to the subdued inflation that much of the world enjoyed before the twin shocks of Covid-19 and the war in Ukraine — or the end of monetary tightening anytime soon.

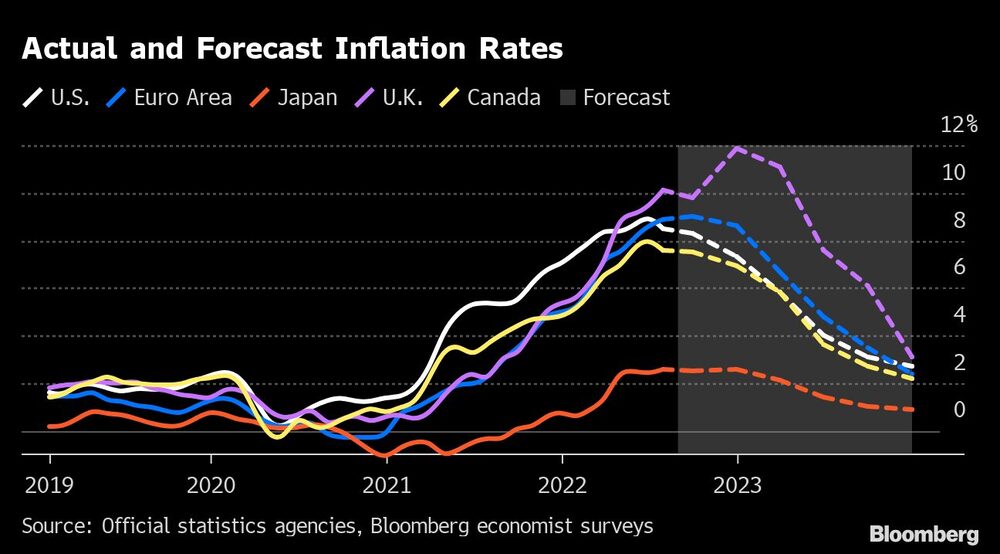

Fed’s Still Hiking

Rents and labor-intensive services are likely to keep getting more expensive, with job markets tight and wages on the rise. And there are broader forces at work, from slowing globalization to lackluster growth in the labor force, that may keep price pressures bubbling.

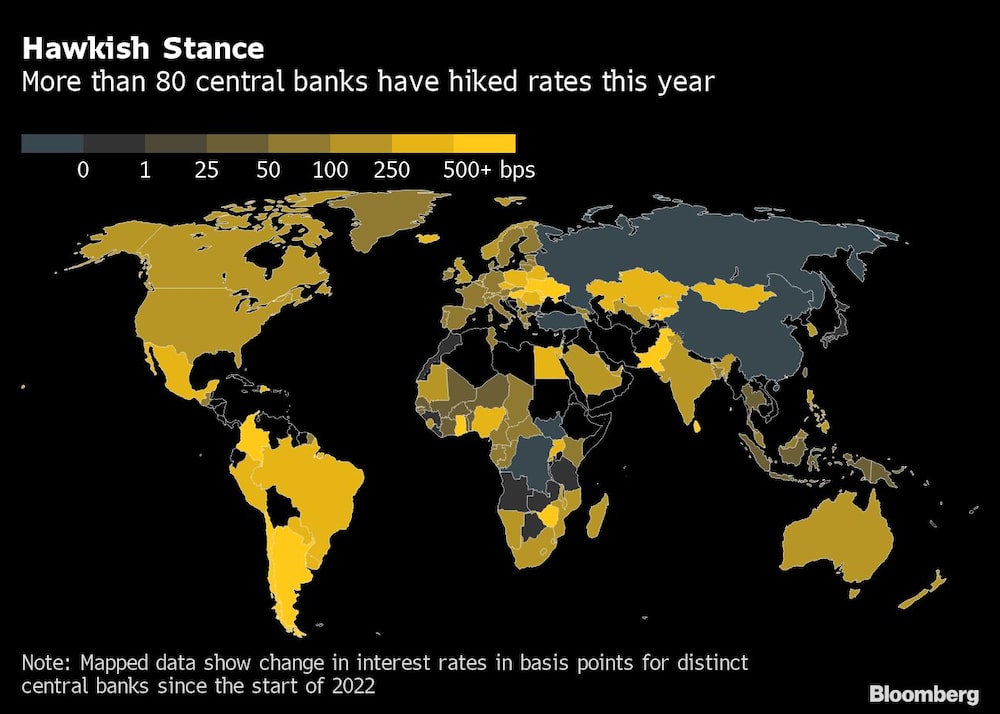

The major global central banks, which failed to see the pandemic price shock coming, are set to press ahead with interest-rate increases even as headline inflation tops out. The Federal Reserve, European Central Bank and Bank of England are all expected to hike rates again in September.

Fed Chair Jerome Powell left the door open to another jumbo 75 basis-point increase next month, telling fellow central bankers in Jackson Hole on Friday that a recent ebbing of US inflation “falls far short” of what policy makers want to see.The following day, ECB Executive Board member Isabel Schnabel said “central banks need to act forcefully.”

Some central banks that were quicker off the mark than the Fed to raise rates may take advantage of cooling price pressures to pause their tightening moves.

The Czech National Bank this month left policy unchanged while the Brazilian central bank is expected to do the same in September. And New Zealand’s Reserve Bank may be nearing the end of its aggressive moves, Governor Adrian Orr told Bloomberg Television from Jackson Hole.

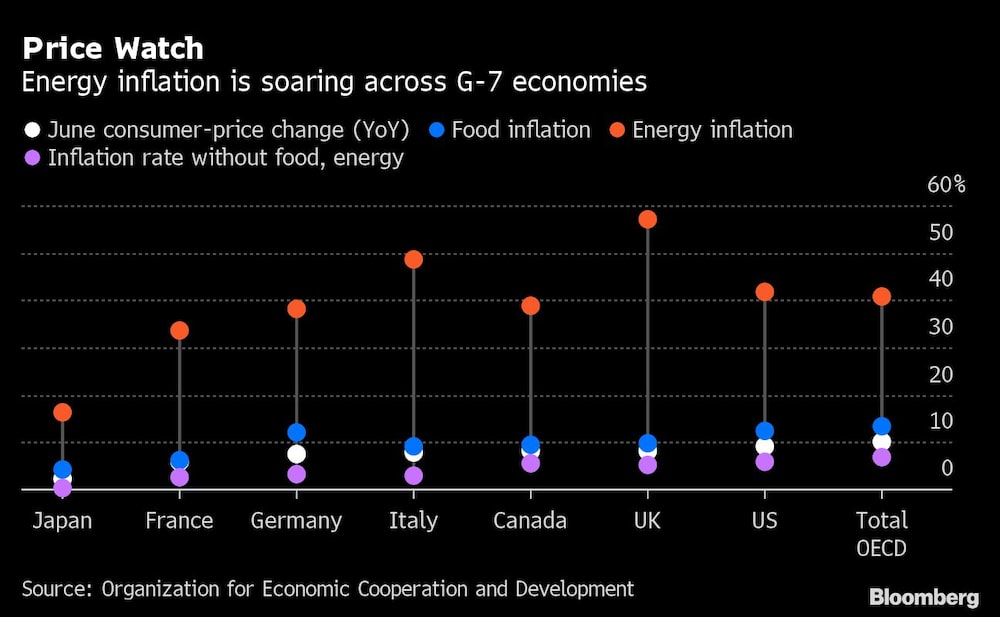

The soaring cost of living has left politicians as well as central bankers feeling the heat — especially in Europe, where natural gas prices more than seven times higher than a year ago have triggered an energy emergency.

Inflation in the euro area is forecast to accelerate beyond July’s record 8.9% and Citigroup Inc. predicts that it could exceed 18% in the UK, in part because a cap on energy bills just got lifted. All kinds of once-unlikely proposals, from nationalization to power rationing, have been floated to address the crisis.

The US, by contrast, will experience the fastest slide in inflation among developed economies, thanks in part to the strength of the dollar, the JPMorgan economists say.

That won’t stop the Fed from tightening into restrictive territory. Anna Wong, chief US economist at Bloomberg Economics, expects the Fed will eventually have to raise rates as high as 5% to rid the US of its inflation problem.

‘Truly the Issue’

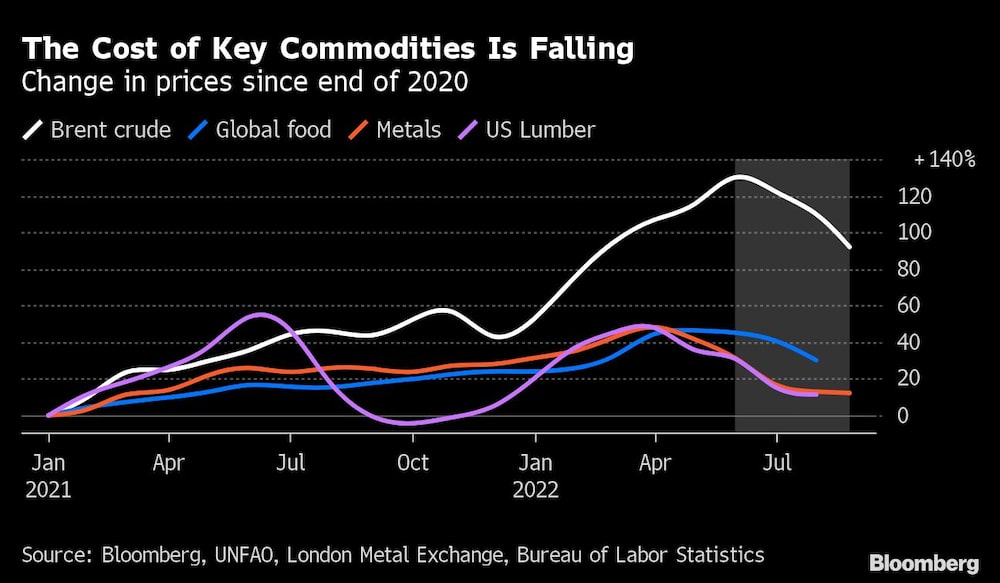

Still, the recent decline in several important commodity markets should help dampen prices across the global economy:

- Benchmark crude oil futures have fallen about 20% since early June

- Prices for metals, lumber and memory chips have declined from their highs

- A United Nations index of food costs plunged almost 9% in July, the most since 2008

Much of this appears to stem from a slackening in demand. That’s partly because consumers are shifting away from the unusual shopping habits that emerged during pandemic lockdowns, when people spent less on services like hotel rooms or gym memberships, and more on goods such as exercise bikes and home computers. Goods inflation “is going to come off a lot,” says Jan Hatzius, chief economist at Goldman Sachs Group Inc.

The turnaround in commodity prices also reflects the fact that household budgets are increasingly stretched — and economies are slowing worldwide.

Most of Europe is expected to fall into recession in the coming months as the energy crisis takes a toll over the winter. China remains hobbled by its Covid Zero policy and a depressed property market, with spillovers for commodity prices. In the US, Fed rate hikes have undercut the once-ebullient housing market and turned high-tech companies cautious.

Even with recession risks rising, bond investors don’t see central banks letting up in the near future. Investors are currently betting that by next March the Fed will have raised rates to around 3.75%, while the ECB’s benchmark will be up to 1.75% and the UK’s to 4%.

“Inflation is truly the issue and it remains well above the targets of central banks,” said John Flahive, head of fixed-income investments at BNY Mellon Wealth Management. “They do not want to make the mistake of lowering rates and watching inflation go back up.’’

‘Seen the Worst’

One sure sign of slowing demand, according to economists at Morgan Stanley, is that growth in imports across major economies — after adjusting for inflation — is now subdued, while exports from Asia, the world’s factory floor, are starting to weaken.

The easing of logistical logjams is also contributing to lower prices. The New York Fed’s index of global supply-chain pressure has dropped to the lowest level since early 2021. Short-term shipping rates are falling, transit times across oceans are shortening, and companies are even starting to moan about bloated inventories.

“We were getting about a 65% service level from our strategic suppliers. That’s back up to a plus 90% now,” Randy Breaux, the president of Motion Industries Inc., an Alabama-based provider of industrial components, told a conference this month. “We really think that we’ve seen the worst of the supply-chain issues.”

If that’s the case, the Fed may not have to raise rates as much as feared to reduce demand and rein in inflation, according to Apollo Management chief economist Torsten Slok.

Still, even if goods prices slow, there’s a risk that the post-lockdown spending shift will instead drive up the price of services such as going to the movies or staying in hotels. Those may prove stickier.

US rental costs, in particular, are being boosted by a dearth of affordable housing. That may put upward pressure on inflation into 2023 and “maybe even beyond,” Goldman’s Hatzius says.

‘Not Very Far’

Rising wages could also keep inflation around for longer.

Labor costs are by far the biggest expense for many businesses, especially in service industries. With job markets in the US and Europe still tight, companies are being forced to boost pay. To maintain profits, firms would then need to pass along their higher wage bills to consumers.

“We are quite worried about a wage-price spiral,” says Robert Dent, senior US economist at Nomura Securities. “One may already be happening to a certain degree.”

There’s also the argument that inflation won’t return to pre-Covid levels because the world was already poised to change. Globalization is fraying — a process accelerated by the war in Ukraine — and measures to tackle climate change could add another layer of costs, at least in the short term.

In a report this month, economist Dario Perkins of TS Lombard predicted that such forces will combine to create what he calls a “new macro supercycle.”

Central banks “will try to prevent this secular transition, even at the cost of a recession,” but they “can’t stand in the way of structural shifts,” he wrote. “The persistent ‘low-flation’ era is over.”

For now, at least, there’s a growing consensus that the worst of the current inflationary episode is passing for many economies, even if doubt lingers over how fast the decline will be and how far it will go.

“The inflation peak is not very far from here and should be in place soon,” said Priyanka Kishore of Oxford Economics. “There may of course be outliers. But this is more due to idiosyncratic country factors rather than the global price pressures.”

Read more at Bloomberg.com