Bloomberg Línea — The drums of an economic recession are echoing in Latin America as the slowdown is starting to affect the region’s startups, and which have resorted to a wave of layoffs to refocus their businesses.

After accelerating growth in the midst of the pandemic, companies now face a challenging cocktail that mixes a slower economy, higher interest rates and the highest inflation in decades, and companies such as Vtex, Bitso, Klarna, Olist and Buenbit have in recent days announced massive cutbacks to cope with this new scenario.

The outlook, however, is not the same for everyone. David Vélez, CEO and co-founder of Nubank (NU), spoke exclusively to Bloomberg Línea on the sidelines of the Lendit Fintech event in New York this week about the results of the company that has a presence in Brazil, Mexico and Colombia, and his projections for the company this year.

Vélez highlighted the performance the company has had in the markets where it operates, and spoke about Nubank’s bet on cryptocurrencies, saying that he is ‘bullish’ about the future of a technology that he considers disruptive for the financial services ecosystem.

Nubank’s CEO also referred to the political noise ahead of the Colombian presidential elections, the first round of which takes place on May 29, and how the neobank is facing the economic challenges that have led other companies to lay off staff, a move that, Vélez says, Nubank has no need to take.

The following interview was edited for clarity and length.

Bloomberg Línea: Last week you delivered your quarterly results, how did Nubank manage to reverse the losses it reported in the first quarter of 2021?

David Vélez: Our model has a lot of potential for operational leverage. Our sales continue to increase significantly: in the last quarter they grew more than 220%, because our number of customers continues to increase, and the number of products they use continues to increase.

So, all of our sales continue to increase and grow at a very high rate, with a cost that is fixed per number of customers, and which is even going down. That means that that starts to create quite a bit of capacity to generate results, and it’s already getting to a point where there’s enough scale to start to see the power of that business model.

Our first product, which is the credit card, is already profitable after three years. We are investing all that profitability in new products in Brazil.

Brazil as a country is already profitable and we reinvest all that in growth in Mexico and Colombia, and the size of the company is already so large in terms of sales that it can already pay all the expenses while we continue to invest in growth.

Are Mexico and Colombia already profitable? Or when do you expect them to be?

Mexico and Colombia are just starting. It will take time for them to be profitable, but there is so much opportunity that we continue investing a lot in the growth of those markets.

You recently announced the receipt of a $650 million credit line to use in both countries, in what specifically are you going to invest that money?

The credit is mainly to finance capital requirements that we need for credit cards in Colombia and Mexico.

Are you planning to launch new products in those countries?

I can’t confirm that yet, but yes, obviously in the long term we have the idea to increase the number of products we are offering.

What is your customer target number for 2022 in the three countries in which you operate?

I can’t give your a specific target.

, participated in the Lendit Fintech forum in New York this week, and talked about how the company started out and the challenges it has faced. Photo: Bloomberg Línea")

How much could Nubank be hit by the economic environment we are in, with the combination of higher inflation and higher interest rates? Could your access to credit be affected?

It’s interesting, because the environment we are experiencing today of high interest rates and high inflation is actually even more benign than the environment we have seen as a company since 2013. In Brazil, they are forecasting 1% GDP growth, another 1% next year. That’s better than virtually every year in which we’ve been operating.

“We have to raise interest rates, our funding cost goes up, so we have to raise interest rates to users in the same way.”

David Vélez, CEO of Nubank

Our history as a company has always been amidst very difficult scenarios. We saw a 7% GDP contraction in one year in 2017; the worst recession in Brazil in 100 years; we saw the pandemic; we saw impeachment; we saw political crises. So, the scenario we see today is significantly better than any scenario we have seen in the past.

So you are hopeful that the growth you’ve talked about will continue despite this scenario?

Yes, we definitely see an opportunity for continued growth. There are certain areas of our portfolio where we want to be more conservative, and we are stopping some origination, but in general we expect to see an environment of a lot of growth, mainly because a lot of our growth is taking on people who have a very good credit history, who leave their banks and come to Nubank.

So, we are able to pick the customers that have the best credit history, and give them a credit opportunity. We are not yet seeing customers who never had a credit history, so we can continue to grow quite a bit within a customer base that already had those types of services.

You recently launched a cryptocurrency service in Brazil, why this interest in this industry, and would you also consider bringing it to the other two markets where you are operating?

We have seen over the last 12 to 24 months a lot of interest within our consumer base for crypto. Basically, we can see money coming out of savings accounts, going into cryptocurrency platforms in Brazil. It’s a product that has a lot of interest.

As a company, we are very ‘bullish’ on the future of crypto, being quite a disruptive technology for the future of financial services. We want to serve our clients with crypto options, and we also want as a company to prepare for a future where crypto is going to be one of the most disruptive technologies in the world.

Do you have balance sheet exposure to cryptocurrencies?

We’ve announced that within our balance sheet we are going to have up to 1%. In our case, in Bitcoin.

And how much is it now?

I cannot give you that number specifically.

Although the percentage is tiny, doesn’t it represent a risk, due to the volatility of crypto assets?

Yes, it has more volatility than the other 99% of our cash. But, in the long term, we are very confident that it is a good investment.

Do you see an environment in which to bring this service to Mexico and Colombia? Because they are also countries where the crypto industry is moving a lot...

Definitely. We do not yet have a clear plan of when that would be, but we are also interested at some point.

You tell me that the scenario is even less challenging than what you are used to. But could this increase in interest rates in Brazil, Mexico and Colombia affect the interest rates you offer to your users?

Yes, we have to raise interest rates, our funding cost goes up, so we have to raise interest rates to users in the same way. That is what we have had to do. Anyway, we generally try to have much lower rates than the banks. In Brazil, we are 20-30% below the banks. In Colombia as well and, even though we have to raise interest rates, we still plan to maintain a more aggressive and more consumer-friendly positioning of keeping lower rates.

“I think the market has changed a little and now many people are less interested in investing in technology companies and more in traditional ones. It’s a pendulum that always swings. But it is more momentary”

David Vélez, CEO of Nubank

In recent weeks there has been a wave of layoffs in Latin American startups. Many cite the macroeconomic situation, why is this happening? Is Nubank unaffected by this phenomenon?

I believe that crises are moments when companies have to become more efficient. All companies grew a lot during the pandemic and there is always an opportunity to become more efficient and see where costs are going. So we are looking carefully at what opportunities we have to increase our operational efficiency and trying to cut unnecessary expenses.

That said, we don’t see any need to make any layoffs. We have invested a lot in our employees, we have a very strong team, and in fact we are continuing to hire a lot of people this year and growing quite a bit.

We are in a very strong position after our IPO, where we raised over $2.8 billion, we have more than another $1 billion in cash. The company is basically in a break-even moment, so we see it as a time to really accelerate and that’s why we want to make sure that we keep one of the best teams in Latin America, engaged and excited to be working with us.

that were not able to sell their shares immediately after the company carried out the IPO.")

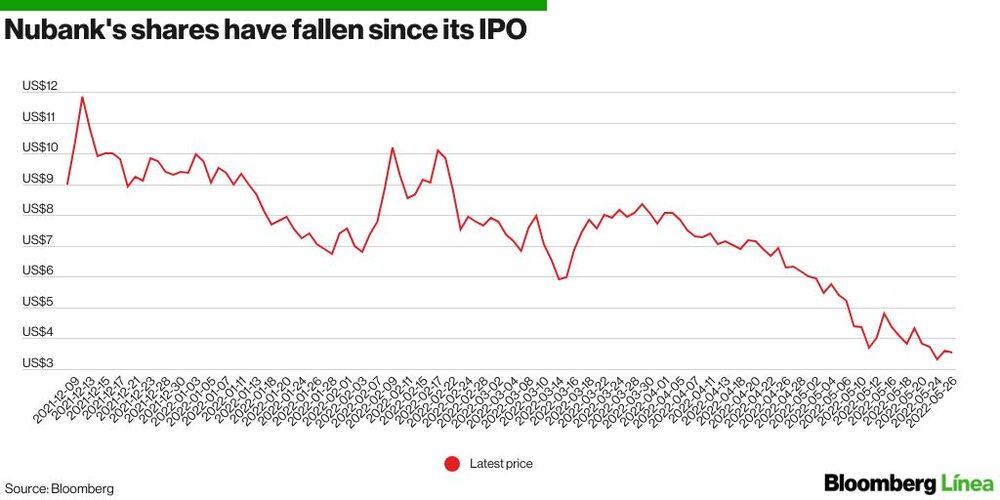

There was a lot of talk that when the lock-up period on the sale of shares after the IPO was over, that there could be a massive sale...

Yes, we had a lot of investors who had invested since our seed round, who have been with us for seven or nine years, and at some point they have to provide liquidity to their investors. There was a rumor that they were all going to sell. We went to talk to basically all of them and basically all of them said no, that they are keeping their shares for the long term.

In fact, many of them are buying shares right now, but there are some that do have to provide liquidity, there are some that do have to take advantage, for some internal reason, they have to decide to pass on those shares. So yes there have been shareholder sales, that has contributed to the stock dropping, there has been pressure, but our core investors are with us for a longer period of time. And in fact, they are again taking the opportunity to buy.

Are you looking for more investors?

No, we are not looking for new investors. Maybe what is affecting us is how many people are coming in to buy the stock. I think the market has changed a little bit and now many people are less interested in investing in technology companies and more in traditional companies. That’s a pendulum that always swings. They are cyclical, and that is why from one moment to another technology companies were a little bit more affected. But it is something very momentary.

Still, if you ask yourself where you would prefer to invest in the long term, what is the stock that you would like to have five or ten years from now, I have no doubt that the best opportunity are companies that are reinventing all industries and are disruptive companies that are competing. So, in the short term there’s going to be a lot of volatility. It’s going to go up, it’s going to go down. We really don’t care, we are super focused on the long term and we believe that the long term opportunity is gigantic.

From June 1, the stock will be available on the Colombian stock exchange through the Global Market, why did you decide to take this step?

We want our clients to be our partners. It is something we did in Brazil at the beginning when we allowed our clients to invest in the IPO, and we even gave away a share to more than seven and a half million of our clients. It’s a way of aligning incentives. So, we really like that alignment of interests and having the opportunity for Colombians to get into the same boat and be part of our dream. That’s a great way to increase loyalty.

“All these governments, regardless of their political vision, have always agreed that more competition to the banking oligopoly is good for the consumer, that lower prices are better for the consumer, that more financial inclusion is good for the consumer.”

David Vélez, CEO of Nubank

Again, it’s a long-term investment. You can’t go in there thinking you’re going to have to buy overnight. That’s not what I would recommend. But Colombia is a priority for us. We are very happy so far with the growth we have seen. We already have more than one million Colombians on the waiting list and more than 200,000 using our services, so we are prepared to continue investing in the country.

You are present in two countries with presidential elections coming up this year, Colombia and Brazil. How much does the political noise affect investments?

It doesn’t really worry us, it doesn’t affect us. Since we started in 2013 we have worked with clients, with governments in Brazil, Mexico and Colombia of all types. Some right-wing governments, some left-wing governments. All these governments, regardless of their political vision, have always agreed that more competition to the banking oligopoly is good for the consumer, that lower prices are better for the consumer, that more financial inclusion is good for the consumer. So, given our mission to increase fair and better financial access, it’s an issue that has always had a lot of support from any government. So, from that point of view, we are not really concerned about it.