in Davos, Switzerland, on Sunday, Jan. 15, 2023.")

Bloomberg — Chinese data may reveal damage to the economy from Covid lockdowns, US retail sales could show a further decline, and UK inflation is likely to slow. Central bankers in Malaysia and Indonesia are expected to hike rates, while Norway and Turkey are likely to hold, and Angola may cut.

Latin America

In a light week for indicators in the region, Brazil’s central bank leads off with its closely watched Focus survey of local economists’ expectations.

Notably, last week’s survey showed that while Banco Central do Brasil did bring down inflation by more than 600 basis points in 2022, economists expect only scant deceleration in 2023 and don’t see the headline rate back to target before 2026.

In Mexico, data on retail sales and same-store sales are likely to show some bounce thanks to end-of-year bonuses and a major shopping there holiday akin to Black Friday.

In Colombia, a raft of indicators will likely underscore the increasing drag on the economy from double-digit inflation and interest rates. From a 10.6% expansion in 2021, economists surveyed by Bloomberg forecast the economy’s cooling in the fourth quarter to slow 2022 growth to 7.7% overall, on the way to a far lower 1.3% pace projected for 2023.

Back in Brazil, the national unemployment rate in November may have declined for an 18th time in 20 months after hitting a seven-year low of 8.3% in October. Analyst estimates range from 7.9% to 8.4%, quite possibly below the level where the labor market begins to impact inflation.

World Economic Forum will resume normal business with its first winter meetings in Davos, Switzerland, since before the pandemic.

US and Canada

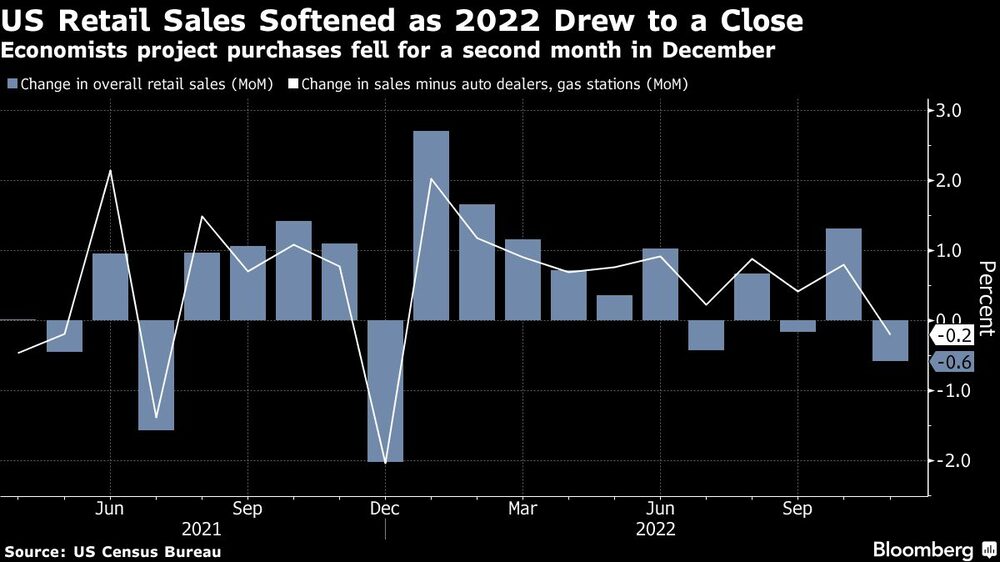

After the latest consumer-price data showed US inflation is moderating, attention this coming week turns to demand, with Wednesday’s release of December retail sales figures.

Purchases are seen retreating for a second month, reflecting weaker vehicle sales and a drop in receipts at gasoline stations. Sales are also seen declining for consecutive months when autos and gasoline are excluded. The figures aren’t adjusted for inflation.

Other reports on Wednesday include the producer price index and industrial production. Economists forecast a further moderation in prices paid to producers in December.

Output at manufacturers, utilities and mines probably stagnated last month, restrained by a second straight drop in factory production. Data in the latter part of the week is projected to show a decline in housing starts and sales of previously owned homes at the end of 2022.

Further north, the last major inputs into Bank of Canada Governor Tiff Macklem’s first policy decision of the year will be released.

The central bank publishes quarterly business and consumer outlook surveys on Monday. Policy makers are watching inflation and wage expectations as they weigh whether to pause their aggressive campaign of rate hikes on Jan. 25.

Consumer price index data for December, due Tuesday, may firm up bets for another 25-basis-point increase after a blowout jobs report. Headline inflation in Canada is expected to ease to 6.3%, but core measures may show underlying pressures.

Asia

The Bank of Japan returns to the spotlight this week after it shocked global financial markets in December with a tweak to its stimulus program.

While all but one of 43 economists in a survey forecast the central bank to leave policy unchanged on Wednesday, many say they can’t rule out more action.

That’s partly because the BOJ’s messaging has become less clear following its doubling of a cap on 10-year bond yields. Governor Haruhiko Kuroda in the past has characterized such a move as a rate hike, but last month said it was aimed at improving the sustainability of its stimulus framework.

He’ll step down in April, and speculation is building that the central bank will then move toward a normalization of policy.

Despite the decision to allow wider bond movements, pressure on the BOJ’s yield curve control framework has only increased since last month.

Japan’s 10-year yield rose above the new ceiling of 0.5% Friday for the first time since the Dec. 20 gathering, prompting the BOJ to shell out 3.2 trillion yen ($24.9 billion) on fixed-rate bond purchases to rein it in — a daily record.

Traders are now even more convinced that any change in the policy must be a surprise, making the January meeting a wild-card. Citigroup economists expect the bank to scrap its yield curve control entirely.

A local media report on Thursday said the central bank will assess the side effects of its large-scale monetary easing, fueling further speculative moves by investors.

Still, BOJ officials see little need to rush through another big move to improve bond- market functioning, and policy makers should assess the impact of last month’s yield adjustments for now, people familiar with the matter told Bloomberg earlier this month.

New quarterly economic projections released along with a policy statement will also come under scrutiny. They’re widely expected to show a higher outlook for prices in the coming fiscal years. Inflation data due on Friday may show acceleration too.

What Bloomberg Economics Says:

- “To push back against market pressure for an earlier move to normalize policy, we think the BOJ could announce that it will carefully watch yen swap rates — in a new jawboning tactic.” —Yuki Masujima, senior economist

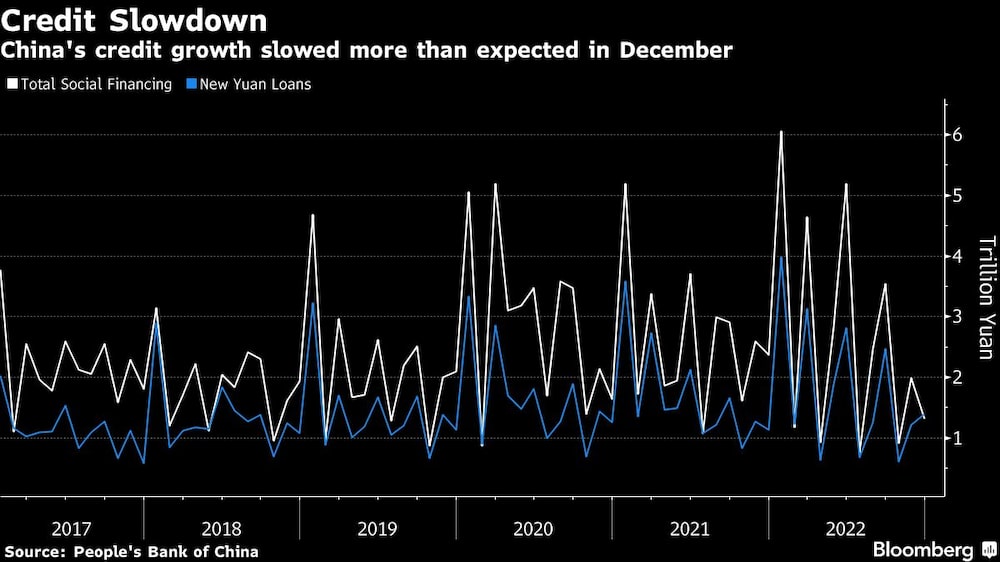

Elsewhere in Asia, China releases retail sales, investment and industrial output numbers for December on Tuesday, with downbeat figures expected as Covid’s spread dented confidence in the final weeks of 2022.

Fourth quarter and full-year GDP data will show an economy that slowed under the weight of Covid restrictions and a property downturn, though attention is rapidly shifting toward prospects for a recovery as China’s economy reopens.

Down Under, jobs figures will indicate how the economy is faring as the Reserve Bank of Australia mulls whether to continue or pause its tightening cycle.

Bangladesh’s central bank on Sunday raised the benchmark rate by 25 basis points, its fourth straight interest rate hike.

In Southeast Asia, Indonesia and Malaysia may continue raising rates at meetings on Thursday.

Europe, Middle East, Africa

UK data will take center stage in European markets. On Tuesday, jobs and wage numbers will allow the Bank of England to gauge how price gains are feeding into the labor market. Inflation data the next day may have slowed closer toward 10%, raising the prospect that the worst has passed.

The BOE releases its survey of credit conditions on Thursday, and the week will finish with retail sales for December — expected to show a rebound from the previous month at a calendar high point for spending. That may support the gist of data last week suggesting the UK may have avoided falling into a recession.

The main BOE appearance for the week will be Governor Andrew Bailey and colleagues on Monday, testifying to Parliament’s Treasury Committee.

In the euro zone, minutes of the European Central Bank’s December rate decision on Thursday will be a highlight. Policy makers including President Christine Lagarde are also due to speak, with most doing so in Davos.

More than 2,700 members of the global elite plan to gather at the Swiss resort for the World Economic Forum. Swiss National Bank President Thomas Jordan will also speak there.

Elsewhere in Europe, Norway’s central bank on Thursday is likely to keep its benchmark rate unchanged at 2.75% and repeat guidance for one more quarter-point hike in March.

The same day in Turkey, policy makers will probably hold rates steady for a second month, having brought the benchmark into single digits as demanded by President Recep Tayyip Erdogan. But with general elections now months away, more cuts could be on the cards — even as inflation remains above 60%.

The region’s final decision of the week will be in Angola, where the central bank may add to the one rate cut it delivered last year after inflation slowed in almost every month of 2022.

South African data on Wednesday may show inflation exceeded 6%, the upper limit of the central bank’s target range, for a seventh straight month. That may be enough to prompt the eighth rate hike since November 2021 the following week.

--With assistance from Vince Golle, Benjamin Harvey, Robert Jameson, Malcolm Scott and Stephen Wicary

Read more on Bloomberg.com