A roundup of Monday’s stock market results from across the region

👑 Argentina leads in Latin America:

Argentina’s (MERVAL) was the only Latin American index to close with gains on Monday, ending the day 0.34% higher, with the biggest gains seen by the shares of Aluar Aluminio (ALUA) and Banco BBVA Argentina S.A. (BBAR), which closed 3.28% and 3.18% higher, respectively.

The so-called ‘soybean dollar’ was relaunched in Argentina on Monday, establishing an exchange rate of 230 Argentine pesos to the US dollar for producers, a measure that will be in force until the end of the year. At the same time, the government will seek to renew maturities for 261 billion pesos through debt bids, in a bid to obtain extra financing.

📉 Peru’s stock exchange sees the sharpest losses:

Peru’s S&P/BVL (SPBLPGPT) led the losses in Latin America, closing 2.11% lower, while Colombia’s COLCAP dropped 1.99%.

The shares of Aenza S.A.A. (AENZAC1) dropped 20% and those of Credicorp Capital Perú S.A. (CRECAPC1) 3.84%, dragging down the Peruvian index amid a tense poltiical situation in the country amid the resignation of prime minister Aníbal Torres and the arrival of Betssy Chávez as head of the cabinet.

Mexico’s S&P/BMV IPC (MEXBOL) closed 1.14% lower, el lunes, following a lackluster performance in the communication services and materials sectors.

Bets on the Mexican peso on the Chicago Mercantile Exchange (CME) slowed, after four weeks of increases, when speculators reduced positions due to the appreciation of the local currency, although it remains at its highest level since March 2020.

Chile’s IPSA (IPSA) and Brazil’s Ibovespa (IBOV) also closed lower, down 0.80% and 0.18% respectively.

🗽 On Wall Street:

US stocks sank on Monday as Federal Reserve officials stressed that more rate hikes are coming, with risk appetite also hit by uncertainties around China’s Covid curbs and their impact on the global economy.

The S&P 500 pared its monthly gain as Fed Bank of St. Louis President James Bullard said markets may be underestimating the chances of higher rates while his New York counterpart John Williams noted policymakers have more work to do to curb inflation. Fed Vice Chair Lael Brainard said the string of supply shocks is keeping inflation risks elevated.

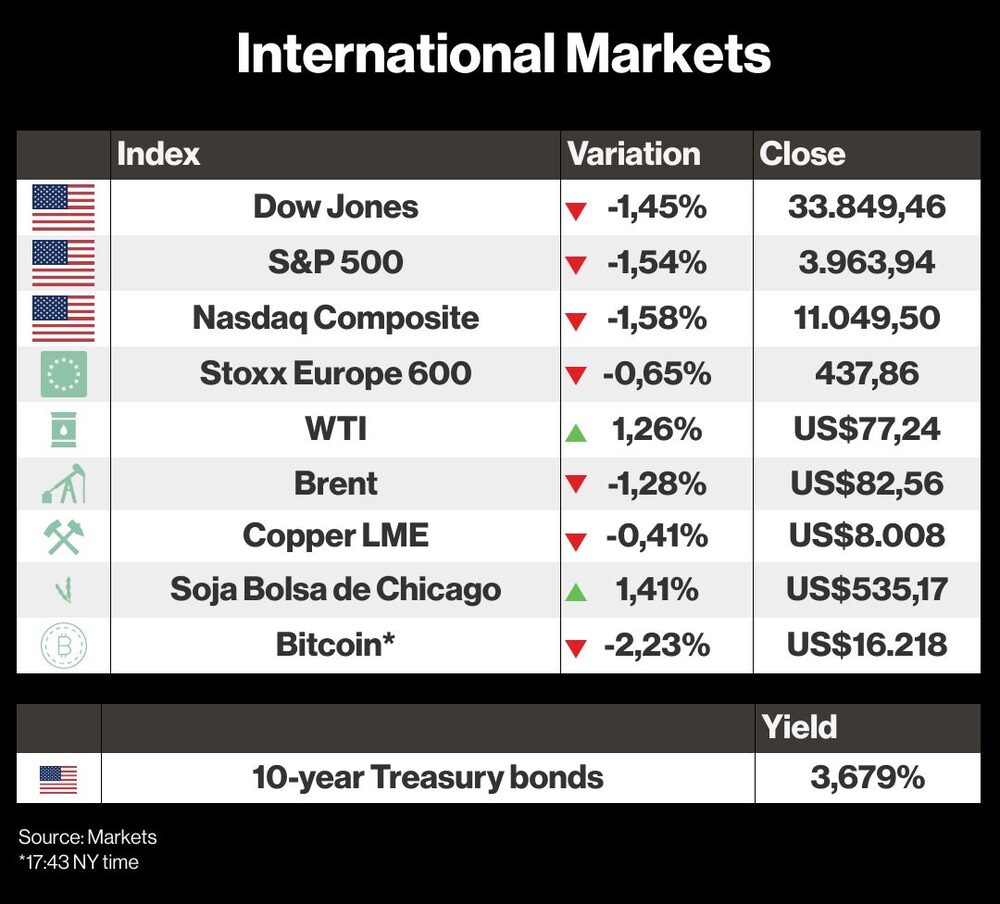

The Nasdaq Composite (CCMPDL) dropped 1.58%, the S&P 500 1.54% and the Dow Jones Industrial Average 1.45%.

Investors are now looking ahead to Jerome Powell’s speech Wednesday, with many economists expecting he’ll cement bets that the Fed will slow its pace of rate increases next month -- while reminding Americans that its fight against inflation will run into 2023.

“We expect Powell will push back more narrowly on market bets on early rate cuts that have once again crept a bit too far into 23, emphasizing that a stronger-for-longer labor market suggests that rates will need to be higher for longer,” wrote Krishna Guha, vice chairman of Evercore ISI.

As traders sought safety, the dollar rose alongside the Japanese yen. Investor anxiety also hit Bitcoin, with the crypto market digesting BlockFi Inc.’s bankruptcy filling. US-listed Chinese shares rebounded from a selloff. Apple Inc. (AAPL) slid as Bloomberg News reported that turmoil in China is likely to result in a production shortfall of close to 6 million iPhone Pro units this year.

China’s woes complicate expectations of its path to reopening, with authorities deploying a heavy police presence in Beijing and Shanghai to deter a repeat of the weekend’s demonstrations. Chances are growing of a messy exit from the Covid Zero policy, analysts at Goldman Sachs Group Inc. warned.

“This is going to keep economic activity subdued in the country, and beyond,” said Fawad Razaqzada, market analyst at City Index and Forex.com. “The civil unrest is adding another layer of uncertainty over the economic situation there. It is certainly hurting investor sentiment across the financial markets.”

Just when the S&P 500 was trying to break above the highs of mid-November, sentiment turned negative, threatening the market’s recent momentum. Timing is most inconvenient here as the index approaches a crucial technical zone in the shape of both the 2022 downtrend and the 200-day moving average. Should the recent bullishness evaporate, short-term tactical bear trades might spark a bout of profit taking.

Stock markets are in for a wild ride next year as they don’t yet reflect the risk of a US recession, according to strategists at Goldman Sachs and Deutsche Bank. Their calls are a warning after equities rallied sharply in the past two months on bets that a peak in inflation will lead to a softening of hawkish central bank policies.

BlackRock Inc.’s Chief Investment Officer Rick Rieder sees a chance for rates volatility to turn lower and provide a necessary, “though perhaps not sufficient” condition for stabilization in risk assets markets.

Stagflation is the key risk for the global economy in 2023, according to investors who said hopes of a rally in markets are premature following this year’s brutal selloff. Almost half of the 388 respondents to the latest MLIV Pulse survey said a scenario where growth continues to slow while inflation remains elevated will dominate globally next year.

On the currency markets, the Bloomberg Dollar Spot Index rose 0.6%, the euro fell 0.6% to $1.0336, the British pound fell 1.2% to $1.1949 and the Japanese yen rose 0.2% to 138.93 per dollar.

🔑 The day’s key events:

WTI crude oil for January delivery made a brief recovery, increasing its price by 1.46% to $77.24 per barrel, while the Brent benchmark for January settlement fell 1.39% to $82.47 per barrel.

Although the Covid-19 advance in China continues to threaten crude oil demand, OPEC+ delegates indicated that cutting production at their meeting next weekend could be a scenario, making WTI gain ground. Meanwhile, European Union discussions to set a cap on Russian oil exports remain stalled.

Cryptocurrencies also had an eventful start to the week. Crypto lender BlockFi filed for bankruptcy in the US, as part of the effects on the industry of the FTX collapse.

As a result, bitcoin (XBT) fell as much as more than 3% on the day, with the value having been just above $16,200, while ether (XET) was down 4%.

🍝 For the dinner table debate:

Elon Musk said Monday that Apple has cut its ad spending at Twitter and has even threatened to pull the app from its app store, signaling a potential battle between the two companies.

“Apple has mostly stopped its advertising on Twitter,” Musk tweeted Monday. “Do they hate free speech in America?”. He then posted again and included Apple CEO Tim Cook’s Twitter account. “What’s going on here?” he said in that tweet.

Minutes later he wrote that Apple could remove Twitter from its store and that “they don’t tell them why.”

Several companies have paused their postings on the social network since Musk’s purchase of the social media company last month. Musk said that led to a significant drop in revenue. Since the purchase, Musk has cut thousands of jobs, raising fears that Twitter will not be able to combat hate speech and misinformation.

Sebastián Osorio Idárraga, a content producer at Bloomberg Línea, and Rita Nazareth of Bloomberg News, contributed to this report.